![]()

Fisher’s Separation Theorem: Why Maximizing NPV Is the CEO’s Only Duty

In the world of corporate finance, few concepts are as powerful—or as liberating for a manager—as Fisher’s Separation Theorem. Imagine you are the CEO of a startup sitting on a pile of cash. You are immediately faced with a conflict: Director A wants a dividend today to buy a yacht, while Director B wants to reinvest the money for long-term growth. Whose side do you take? According to the Net Present Value (NPV) rule, the answer is neither. You follow the math.

This post explores how Fisher’s Separation Theorem proves that a firm’s investment decisions should remain completely independent of its shareholders’ individual consumption preferences. By the end, you will understand why maximizing NPV is the financial mechanism that allows every shareholder to get exactly what they want, when they want it.

What is Fisher’s Separation Theorem?

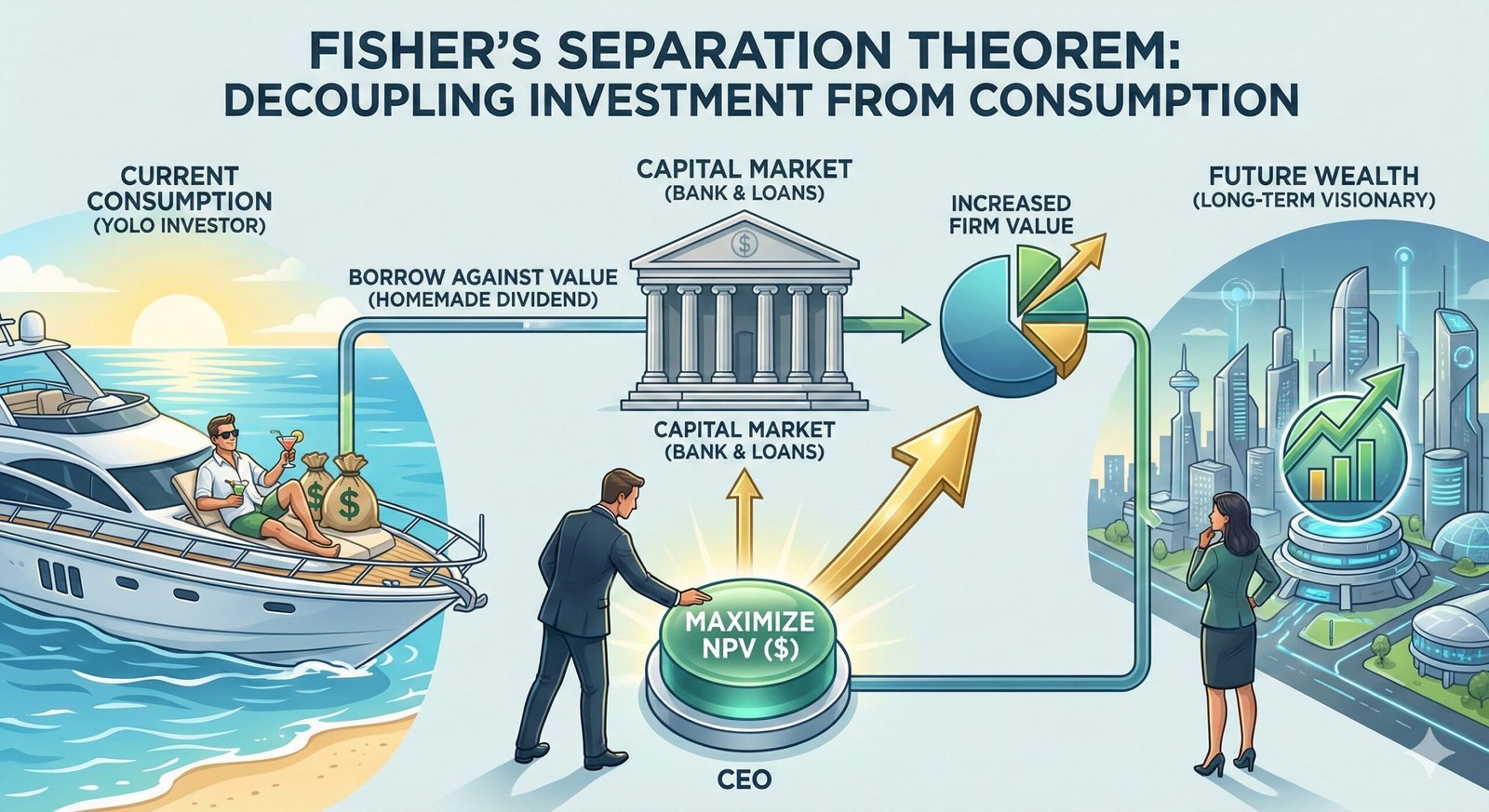

Named after the economist Irving Fisher, this theorem provides a “magical” solution that resolves the conflict between our two directors. Simply put, the theorem states that a firm’s investment decision should be completely separate from the consumption preferences of its owners .

The theorem implies that a corporation does not need to worry about whether its shareholders want to spend money today or save it for tomorrow. As long as the capital markets are functioning , the manager has only one job: to maximize the Net Present Value (NPV) of the firm’s investments.

In this post, we will walk through a simple numerical example to prove why listening to neither director—and instead focusing solely on value creation—is actually the best way to make both of them happy.

The Scenario: The Clash in the Boardroom

Let’s set the stage with a concrete example.

You are the CEO of FutureCorp. The company currently sits on $10 million in cash. You have no debt, and for the sake of simplicity, let’s assume this cash represents the entire value of the firm.

You are facing a critical decision regarding a new opportunity: “Project Supernova.”

The Investment Opportunity (The Project)

- Cost (\(C_0\)): The project requires an upfront investment of *\$10 million* today. (This would use up all your current cash).

- Payoff (\(C_1\)): The project is guaranteed to generate *\$12.1 million* exactly one year from now.

The Capital Market

- Interest Rate (\(r\)): The current market interest rate for both borrowing and lending is *10%*.

The Conflict

Your two major shareholders have radically different plans for their money:

- Director A (The “Spender”): He is impatient. He wants you to pay out the $10 million as a dividend today so he can buy a luxury yacht immediately. He sees “Project Supernova” as a waste of time because he doesn’t want to wait a year for his money.

- Director B (The “Saver”): She is patient. She wants you to take the project because 12.1 million is numerically larger than 10 million. She is happy to wait a year to maximize her wealth.

The CEO’s Problem

If you reject the project and pay dividends, Director A is happy, but Director B is upset that you left money on the table.

If you accept the project, Director B is happy, but Director A is furious because his cash is locked up for a year.

It looks like a zero-sum game. But is it?

The Analysis: The Mathematics of Wealth

Before we worry about who wants money when, we need to answer a purely financial question: Does “Project Supernova” create value?

To find out, we use the Net Present Value (NPV) rule. We need to translate the future payoff of the project into today’s dollars so we can compare apples to apples .

Step 1: Calculate the Present Value (PV)

The project pays $12.1 million in one year. Since the market interest rate is 10%, we discount that future cash flow back to the present:

$$

PV = \frac{\$12.1 \text{ million}}{(1 + 0.10)} = \$11 \text{ million}

$$

Step 2: Calculate the Net Present Value (NPV)

Now, we subtract the cost of the investment from the present value of its payoff:

$$

NPV = PV (\text{Benefits}) – PV (\text{Costs})

$$

$$

NPV = \$11 \text{ million} – \$10 \text{ million} = \mathbf{+\$1 \text{ million}}

$$

The Verdict:

By taking this project, you are instantly increasing the value of the firm by $1 million.

- Scenario A (Reject Project): The firm is worth $10 million (the cash on hand).

- Scenario B (Accept Project): The firm is worth $11 million (the present value of the future cash flow).

The math is undeniable. Scenario B makes the shareholders richer.

“But wait,” you might say. “Director A doesn’t care about being ‘richer on paper.’ He wants cash in his pocket today to buy his yacht. Investing in the project locks up his money for a year!”

This is where the power of Fisher’s Separation Theorem kicks in.

The theorem tells us that because capital markets exist (banks, loans, etc.), consumption decisions are separate from investment decisions .

Director A is making a mistake by conflating the firm’s cash flow with his personal cash flow. As we will see in the final section, he can actually buy a better yacht by letting you invest in the project.

The Solution: Creating Your Own Payday

This is the part where Director A usually gets confused. “If you invest the money,” he argues, “I have zero dollars today. I can’t buy my yacht!”

This is where Fisher’s Separation Theorem proves him wrong. It states that as long as Director A has access to the capital market (the bank), he can separate the company’s investment decision from his personal consumption timeline.

Let’s demonstrate how Director A can get his cash today, even if the company invests for tomorrow.

Scenario 1: The “Dividend Now” Approach (What Director A wants)

- You cancel the project and pay out the $10 million as dividends.

- Director A receives: $10 million immediately.

- Result: He buys a $10 million yacht.

Scenario 2: The “NPV Maximization” Approach (What you should do)

- You invest in “Project Supernova.”

- Step 1 (Value Creation): The firm now owns an asset worth 11 million (the present value of next year’s 12.1 million payoff).

- Step 2 (Homemade Dividend): Director A wants cash now. Instead of waiting for the company, he goes to the bank.

- He uses his shares (which claim the future $12.1 million) as collateral to take out a personal loan.

- He borrows exactly the Present Value of the future payout: $11 million.

- Step 3 (Repayment in 1 Year):

- The bank charges 10% interest. Next year, Director A will owe: $$

\$11 \text{ million} \times 1.10 = \$12.1 \text{ million}

$$ - Conveniently, “Project Supernova” pays out exactly $12.1 million next year.

- Director A uses the project payout to pay off the bank loan perfectly.

- The bank charges 10% interest. Next year, Director A will owe: $$

The Final Comparison

| Strategy | Cash Available Today | Future Liability | Net Result |

| 1. Don’t Invest (Dividend) | $10 Million | None | Director A buys a standard yacht. |

| 2. Invest + Borrow | $11 Million | Covered by Project | Director A buys a bigger yacht. |

Conclusion

By investing in the positive NPV project, you essentially created $1 million out of thin air.

- Director A can borrow against this future wealth to spend $11 million today, which is 1 million more than if you had just listened to him in the first place .

- Director B can simply hold her shares and enjoy the $12.1 million next year (which is equal to investing $11 million at 10%).

This is the power of Fisher’s Separation Theorem. It proves that a manager’s only duty is to maximize the firm’s Net Present Value.

- If the firm maximizes wealth (the size of the pie), shareholders can use the capital markets to slice that pie whenever they want to eat it—whether that’s today, tomorrow, or ten years from now .

So, the next time a shareholder demands cash for a personal purchase, tell them: “I’m going to make you rich first. You can go to the bank and get the cash yourself.”